Table of Contents

1. Quick Summary

2. What is DPR for Factory Loan and Subsidy?

3. Why DPR is Important for Factory Loan Approval

4. Step-by-Step Process to Prepare DPR for Factory Loan

5. Documents Required for Factory DPR

6. DPR for Government Subsidy Schemes in India

7. How DPR Helps in PMEGP, CGTMSE & MSME Approval

8. Common Mistakes to Avoid in Factory DPR

9. FAQs

10. Conclusion

2. What is DPR for Factory Loan and Subsidy?

3. Why DPR is Important for Factory Loan Approval

4. Step-by-Step Process to Prepare DPR for Factory Loan

5. Documents Required for Factory DPR

6. DPR for Government Subsidy Schemes in India

7. How DPR Helps in PMEGP, CGTMSE & MSME Approval

8. Common Mistakes to Avoid in Factory DPR

9. FAQs

10. Conclusion

Quick Summary

A detailed project report for factory setup is your gateway to factory funding in India. Whether you're seeking a bank loan, government subsidy through PMEGP, or guarantee coverage under CGTMSE, a well-prepared DPR is non-negotiable.

The DPR should clearly demonstrate:

- Your factory idea is technically feasible

- There's actual market demand for your product

- Your financial projections are realistic and achievable

- You can generate enough cash flow to repay the loan (DSCR of 1.25x minimum)

- You've considered risks and have mitigation strategies

The investment in professional DPR preparation (Rs 10,000-30,000) pays off when it secures a factory loan of Rs 10-50 lakhs or more. It shortens your approval timeline from months to weeks and significantly increases your chances of getting funded.

What is DPR for Factory Loan and Subsidy?

It's a detailed, professional document that explains your entire factory project to lenders and government agencies. It is a formal document that explains everything about your factory and most importantly, how you plan to repay the money. That's exactly why a DPR exists. your business idea, market research, technical details of your machinery, cost breakdowns, financial projections for the next 7-10 years, repayment timelines, and risk assessment. It's basically saying, "Here's my factory plan, here's the money I need, and here's exactly how I'll repay you."

Why DPR is Important for Factory Loan Approval

Here's a hard truth: without a DPR, most factories don't get funded. Banks don't just hand out money based on hope and dreams they need proof, numbers, and a solid plan.

According to official government data, India's MSME loan portfolio has expanded significantly, rising to Rs 64.1 trillion by March 2024 (Source: RBI MSME Report 2024), driven by proper project documentation and financial planning. The government's credit guarantee schemes have approved more than 19.90 lakh guarantees amounting to Rs 2.44 lakh crore during 2024, but most of these approvals are based on well-structured DPRs.

Here's why a DPR matters so much:

- Banks trust numbers more than words: A DPR shows you've done your homework. When you present detailed cost estimates, market research, and financial projections, banks see you as serious.

- It demonstrates viability: Your DPR proves that your factory idea isn't just possible it's profitable. It shows the lender that you've calculated exactly how much money your factory will make.

- It's mandatory for subsidies: Want government subsidies under PMEGP, CGTMSE, or MSME schemes? You need a DPR. Without it, no subsidy. Government rules are clear: the DPR is the trigger for the money.

- It accelerates approval: For a small MSME loan application with all documents ready, the entire process takes just 2-3 weeks. That's because a solid DPR makes approval straightforward.

Have Questions?

How to Make DPR for Factory Loan Step by Step

Here's exactly how to prepare a bankable DPR for a factory loan:

Step 1: Data Collection and Scope Definition

Before you write a single word, gather all your information.

- Promoter details: Your qualification, work experience, and technical knowledge in manufacturing

- Project cost breakdown: It shows how much your building will cost. Your machinery? Your furniture? Your pre-operative expenses?

- Market research data: What's the demand for your product? Who are your competitors?

- Supplier quotes: Get actual quotes for your machinery and raw materials, and banks verify these

- Financial records: Any existing business documents or bank statements

- Location details: it states your factory location, compliance requirements, etc.

This phase typically takes 1-2 days and is critical because accurate data equals accurate projections.

Step 2: Market Analysis and Feasibility Assessment

Your DPR must prove that there's actual demand for your product. This is where you explain the market opportunity.

Write about:

- Current market size for your product

- Growth trends in your industry

- Your competitors and what makes you different

- Your target customers and pricing strategy

- Why your factory will succeed

Use real data. If you're setting up a manufacturing unit for steel or textiles, research how many units already exist, their capacities, and where demand gaps exist.

Step 3: Technical Specifications and Machinery Details

This section is crucial for a detailed project report for the factory setup. Banks want to know exactly what machinery you're buying and why. Include:

- List of all machinery with specifications and costs

- Manufacturer details and supplier quotations

- Technology justification: the given detail should be justified, e.g., 'Why this machinery?' Why not cheaper alternatives?

- Plant layout: A diagram showing how your factory will be organised

- Production capacity: How many units will you produce monthly?

- Quality standards: What certifications will your product have?

- Machinery sourcing strategy: Are you buying new or used? Indian or imported?

A DPR for machinery loan in India must show each item with its exact cost, utility, and ROI calculation.

Step 4: Cost Breakdown and Financial Estimates

This is where numbers speak louder than words.

Your DPR must show:

- Fixed capital costs: Building, machinery, equipment, furniture

- Pre-operative expenses: Licenses, permits, staff training, initial raw material

- Working capital: Money needed to run daily operations

- Contingency margin: Extra funds for unexpected expenses (usually 5-10%)

Under PMEGP schemes, subsidies range from 15% to 35% of the project cost, depending on your category (SC/ST, woman entrepreneur, general, etc.).

Step 5: Revenue and Profit Projections

Now, show the bank that your factory will actually turn a profit. This is an important part of any project report for factory loan approval.

For the next 5-7 years, project:

- Monthly/annual production

- Sales revenue

- Operating costs (raw materials, labour, utilities)

- Net profit

- Cash flow

Example projection for a small manufacturing unit:

| Year | Production (Units) | Revenue (Rs) | Operating Cost (Rs) | Net Profit (Rs) |

| Year 1 | 10,000 | 50 Lakhs | 35 Lakhs | 15 Lakhs |

| Year 2 | 15,000 | 75 Lakhs | 48 Lakhs | 27 Lakhs |

| Year 3 | 20,000 | 1 Crore | 60 Lakhs | 40 Lakhs |

Banks look for two critical metrics here:

- DSCR (Debt Service Coverage Ratio): This measures whether your factory's cash flow can cover loan payments. A DSCR of 1.25x to 1.50x is what banks expect. If your DSCR is below 1.0x, the bank will almost certainly reject your loan.

- IRR (Internal Rate of Return): This shows the profitability of your investment. The higher the IRR, the better.

Step 6: Compilation and Professional Formatting

Pull everything together into a polished document. Your final DPR for a bank loan should include:

- Executive summary (1 page overview)

- Promoter profile and qualification

- Project overview and location

- Market analysis

- Technical feasibility and machinery details

- Manufacturing process

- Project cost and funding sources

- Financial projections and cash flow

- Sensitivity analysis (what if sales drop by 20%?)

- Risk assessment and mitigation

- Implementation timeline

- Annexures (quotations, certificates, land documents, etc.)

The format should match your bank's template or the government scheme's requirements (for PMEGP DPR format or CGTMSE loan approval, formats are specified).

Documents Required for Factory DPR Preparation

Before you sit down with your consultant or start writing, gather these documents:

- Academic and technical certificates (if the project cost exceeds Rs 10 lakhs for manufacturing)

- Aadhar card and PAN card of all promoters

- Address proof (utility bill, rent agreement, property deed)

- Experience certificate from previous employers (if relevant)

- SC/ST/OBC certificate (if applicable, for subsidy benefits)

- Registration certificate (if business already exists)

- Land/property ownership documents or a lease agreement

- Supplier quotations for machinery and equipment

- Market research data from authentic sources

- Bank statements (last 6-12 months)

- Udyam registration certificate (for MSME classification)

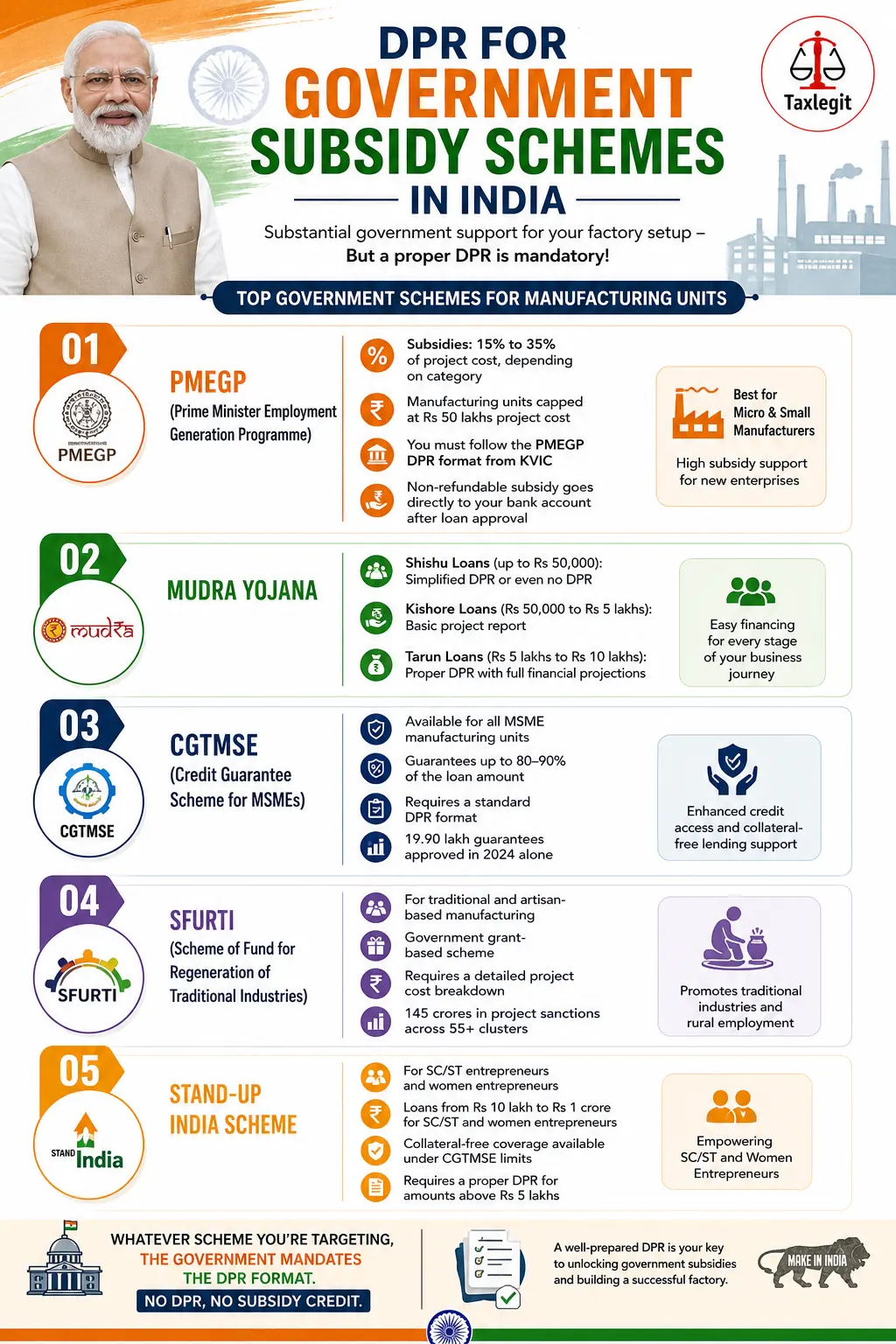

DPR for Government Subsidy Schemes in India

The Indian government offers substantial subsidies for factory setup, but you need the right DPR format. The most common subsidy schemes are:

1. PMEGP (Prime Minister Employment Generation Programme)

- Subsidies: 15% to 35% of project cost, depending on category

- Manufacturing units capped at Rs 50 lakhs project cost

- You must follow the PMEGP DPR format from KVIC

- Non-refundable subsidy goes directly to your bank account after loan approval

2. MUDRA Yojana

- Shishu loans (up to Rs 50,000): Simplified DPR or even no DPR for microenterprises

- Kishore loans (Rs 50,000 to Rs 5 lakhs): Basic project report

- Tarun loans (Rs 5 lakhs to Rs 10 lakhs): Proper DPR with full financial projections

3. CGTMSE (Credit Guarantee Scheme for MSMEs)

- Available for all MSME manufacturing units

- Guarantees up to 80-90% of the loan amount

- Requires a standard DPR format

- 19.90 lakh guarantees approved in 2024 alone

4. SFURTI (Scheme of Fund for Regeneration of Traditional Industries)

- For traditional and artisan-based manufacturing

- Government grant-based scheme

- Requires a detailed project cost breakdown

- 145 crores in project sanctions across 55+ clusters

5. Stand-Up India Scheme

- For SC/ST entrepreneurs and women entrepreneurs

- Loans from Rs 10 lakh to Rs 1 crore for SC/ST and women entrepreneurs. Collateral-free coverage available under CGTMSE limits. Requires a proper DPR for the full loan amount.

- Requires a proper DPR for amounts above Rs 5 lakhs

Whatever scheme you're targeting, the government mandates the DPR format. No DPR, no subsidy credit.

How DPR Helps in PMEGP, CGTMSE, MSME and Subsidy Approval?

This is the practical aspect that really matters to you: let's know about it.

For PMEGP Manufacturing Unit:

Your DPR demonstrates project viability within the scheme's parameters. It shows that your factory investment fits within the Rs 50 lakh cap (for manufacturing), meets technical feasibility, and has market demand. The subsidy ranges from 15% to 35% based on your category. If you're SC/ST or a woman entrepreneur, you get a higher subsidy percentage.

For CGTMSE (MSME Manufacturing Loan):

Your DPR is what convinces the guarantee insurer that your factory is viable enough to warrant an 80-90% loan guarantee. They review your DSCR, IRR, and market analysis to make their decision. A weak DPR gets rejected; a strong one gets approved.

For MSME Registration Benefits:

Once your factory is registered as an MSME using your Udyam account, the DPR helps you access credit limits and subsidised lending rates. The DPR proves your manufacturing credentials to banks.

Have Questions?

Mistakes to Avoid While Preparing Factory DPR

Most DPRs get rejected not because the factory idea is bad, but because of preventable mistakes. Let me list the biggest ones:

1. Underestimating Project Costs

Many entrepreneurs minimize costs to look more profitable. Banks see through this. If your actual machinery costs Rs 10 lakhs but you write Rs 8 lakhs, and the bank approves your loan based on Rs 8 lakhs, you're short Rs 2 lakhs. You'll have to invest out of your own pocket. Get actual supplier quotes.

2. Inflating Revenue Projections

If your factory can realistically produce 100 units per month, don't claim 500. Banks check these numbers with industry experts. Inflated projections kill credibility.

3. Ignoring Market Research

Use authentic secondary data from government sources, industry reports, and trade associations. Banks verify this.

4. Weak DSCR Calculation

If your DSCR falls below 1.0x, your loan gets rejected immediately. This means your factory can't generate enough cash to repay the loan. Recalculate your projections. If DSCR remains weak, either reduce the loan amount or increase projected revenue.

5. Missing Technical Details

Specify brand, model, capacity, and purpose. Show that you've actually researched what equipment you need.

6. Incomplete Documentation

Don't submit a DPR without all required annexures. Missing supplier quotations, certificates, or location documents delay approval.

7. Poor Financial Calculations

Math errors can be costly. Get a CA or financial expert to review your numbers.

8. Ignoring Risk Factors

Don't pretend risks don't exist. Address them. If competition is intense, explain how you differentiate.

Frequently Asked Questions

Q1: Is DPR really mandatory for a factory loan in India?

Yes, for most bank-term loans and for all government subsidy schemes such as PMEGP, CGTMSE, or NABARD, a DPR is mandatory.

Q2: Can I prepare a DPR myself, or do I need a consultant?

You can attempt a basic DPR yourself if you're comfortable with financial documentation and have access to templates (like the PMEGP format from KVIC).

Q3: How long does it take to get a factory loan approved after submitting a DPR?

For MSME loans with a complete, well-prepared DPR and all documents ready, approval typically takes 2-3 weeks.

Q4: What if my factory's DSCR comes out below 1.25x?

A DSCR below 1.25x is problematic because it indicates your factory can't comfortably generate enough cash to repay the loan. Options: (1) Reduce the loan amount you're requesting, (2) Revise revenue projections based on more aggressive marketing, (3) Reduce operating costs, or (4) Increase your own contribution to reduce loan dependence.

Q5: What's the maximum subsidy I can get under PMEGP for a manufacturing unit?

Under PMEGP, subsidies range from 15% to 35% of the project cost, depending on your category. SC/ST/Women/North East/Hill Border area entrepreneurs get 35%; General category gets 25%; Others get 15%. The maximum project cost for manufacturing under PMEGP is Rs 50 lakhs

Conclusion

Setting up a factory is a massive milestone, and your Detailed Project Report (DPR) is the single most important document to get you there. A high-quality, bankable DPR for a factory loan ensures you not only get approval but also maximise your eligibility for PMEGP, CGTMSE, and MSME subsidies.

CTA Don't risk a bank rejection with a generic template. Partner with Taxlegit to get a 100% bank-ready DPR for a factory loan that meets all SIDBI and MSME standards. Secure your capital with confidence.

About the Author

Aabha Garg

Content Writer

Aabha Garg is a TESOL-certified trainer and Lead Content Strategist at Taxlegit with 5+ years of experience. She simplifies complex topics like company registration, GST, and compliance into clear, practical insights for businesses. Reviewed by Vipul Sharma, Co-Founder, Taxlegit.