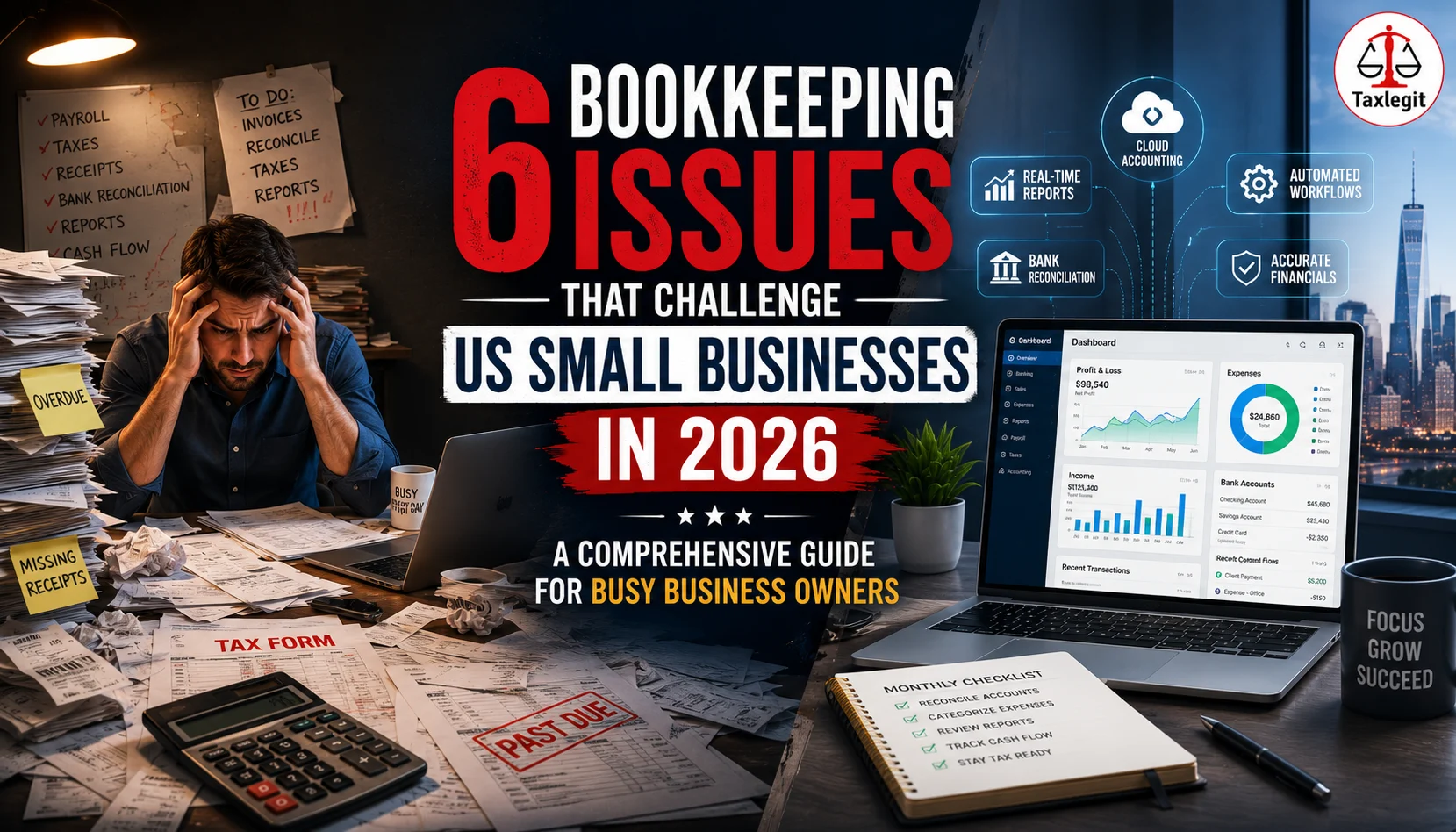

Modern bookkeeping presents a major challenge for US small businesses because founders are forced to juggle sales, client acquisition, payroll, and cash flow tracking simultaneously. In 2026, the six bookkeeping issues that cause the most financial damage are:

- Co-mingling Funds: Mixing personal and business expenses.

- Poor Receipt Tracking: Inefficient digital audit trails.

- Delayed Reconciliations: Postponing bank and credit card matching

- Payroll Inaccuracies: Miscalculating multi-state deductions or contractor vs. employee status.

- Misclassification: Assigning expenses to the wrong tax categories.

- Lack of Real-Time Reporting: Operating blindly without updated cash flow visibility.

The Fix: Transitioning to a streamlined monthly accounting system, deploying cloud-based automation tools, and bringing in fractional professional support long before tax season begins.

Understanding the Back-Office Burden at $1M+ Scale

When you first launch a business, managing the ledger seems straightforward: cash comes in, cash goes out. However, as an enterprise scales past the $1M revenue threshold, back-office operations scale exponentially in complexity.

According to data from the National Small Business Association (NSBA), the average small business owner spends over 120 hours per year solely on federal taxes and compliance. When you add day-to-day transaction tagging, payroll management, and invoice tracking to that workload, accounting quickly transforms from a weekend chore into a full-time operational bottleneck.

Is This Article Written for You?

Meet Sarah. She runs a thriving staffing firm in Dallas generating $1.2M in revenue, managing four employees and seven contractors.

On paper, she’s crushing it. In reality, her bookkeeper quit four months ago, and Sarah has been "temporarily" managing the ledger herself. QuickBooks hasn't been reconciled since February, tax deadlines are creeping up, and that familiar knot of financial anxiety is tightening in her stomach.

If your dashboard looks anything like Sarah’s, take a deep breath. You are not alone.

Falling behind on your books isn't a personal failure it is a predictable, systemic bottleneck that happens to almost every business scaling past the million-dollar mark. The operations outgrew your calendar.

Let’s break down the six most common bookkeeping pitfalls holding businesses back in 2026, and exactly how to fix them without losing your sanity.

| Need Help Cleaning Up Your Books?TaxLegit serves US businesses seamlessly from our global delivery center ensuring your financial stack is handled accurately while you sleep.👉 Click Here to Book a Free Consultation in Your Time Zone Or reach our team directly at: https://taxlegit.com/ |

Why Bookkeeping Becomes a Silent Problem for Small Businesses

In 15+ years of working with business owners, founders, and professional teams, I’ve seen one consistent pattern: most small business owners don’t ignore bookkeeping intentionally. They’re just busy. A restaurant owner is focused on customers. A consultant is focused on client delivery. An e-commerce founder is focused on orders and returns. A staffing firm owner is focused on payroll, invoices, and collections.

Bookkeeping gets attention only when something goes wrong: a tax notice, a cash shortage, missed payroll, a wrong profit calculation, or a CPA asking for documents at the last minute.

At TaxLegit, we believe bookkeeping is not just “data entry.” In fact, it is the financial story of your business. If your books are messy, your decisions become messy too.

Stat #1: Over 20% of US small businesses have received an IRS notice directly linked to bookkeeping mistakes. (Source: The Fino Partners, 2024 Small Business Report)

Stat #2: 65% of small businesses fall behind on bookkeeping in the first half of the year, and the IRS assessed over $1 billion in underpayment penalties in 2024, much of it linked to inaccurate or delayed filings. (Source: Unison Globus / IRS, 2024)

Issue #1: Are You Mixing Personal and Business Expenses Without Realizing the Risk?

Sarah, this one is probably familiar. In the early days, many owners used the same card for business meals, software subscriptions, fuel, office supplies, travel, and personal purchases. It feels harmless at the moment. But it creates a costly mess later.

However, mixing personal and business expenses makes it difficult to know your real profit and defend expenses if the IRS ever audits you.

Real Example: A Dallas-based service firm owner pays for office internet, a client lunch, and personal grocery shopping from the same business credit card. At year-end, the accountant spends four billable hours separating each transaction manually hours that translate directly into higher CPA fees, delayed filings, and increased risk of misreporting.

Issue #2: Do You Have the Right Records to Defend Every Business Expense?

If you are carrying a bank statement alone as proof, it is not enough. Bank statements show that money was spent. They do not prove why the money was spent and for the IRS, the “why” is everything.

For proper bookkeeping and tax support, you need receipts and invoices that confirm the nature of the expense, the vendor name, the date, any tax amount, and the business purpose. The most commonly missing records in small business files:

- Receipts for business meals and client travel

- Vendor invoices for services received

- Software subscription confirmations

- Contractor payment records and signed agreements

- Office supply purchase receipts

- Client reimbursement documentation

TaxLegit Tip: Use a cloud folder or accounting app (QuickBooks, Dext, or even a shared Google Drive) to upload receipts weekly. A five-minute weekly habit prevents a five-day year-end disaster.

Have Questions?

Issue #3: How Long Has It Been Since You Reconciled Your Bank Accounts?

Bank reconciliation means matching your accounting records with your actual bank statement line by line. Many small businesses do this once a year. That’s where the problem begins.

When reconciliation is delayed, small errors compound into large ones. Duplicate entries, missing deposits, unpaid checks, bank charges, failed payments, and incorrect transfers can go unnoticed for months. By the time you catch them, unraveling six months of compounded errors takes far longer than if you’d caught them in the first week.

Real Situation: A staffing firm thinks a client has not paid a $4,200 invoice. An aggressive follow-up call goes out. The payment had, in fact, been received three weeks earlier it simply wasn’t matched in the accounting system. The client is now annoyed. The relationship is strained. The damage was avoidable.

Issue #4: Is Your Payroll Recording Actually Integrated with Your Books?

For US small businesses, payroll errors are among the most expensive mistakes you can make.

| What the data shows: 40% of small to mid-sized businesses face IRS penalties for incorrect payroll filings, with an average penalty of $845 per incident. One in five US payrolls contains an error, and each costs an average of $291 to correct before penalties. Two payroll errors are enough to make 49% of employees start looking for a new job, according to UKG’s 2024 Workforce Report. (Sources: BlinkPayroll/IRS; Valor Payroll Solutions ) |

The most common payroll recording problems in small businesses:

- Wrong employee vs. contractor classification: The DOL’s 2024 Final Rule tightened contractor classification. Misclassifying an employee as a contractor triggers back taxes, interest, and penalties.

- Payroll tax entries missed or delayed: Federal and state payroll tax obligations must be recorded in the books every payroll cycle, not just at year-end.

- Reimbursements not tracked separately: Unrecorded reimbursements inflate apparent payroll costs and distort profitability.

- Payroll software not connected to books: When payroll reports and accounting records don’t match, the reconciliation becomes a quarterly fire drill.

Issue #5: Are Your Expenses Going Into the Right Categories?

Bookkeeping is not only about entering numbers. It’s about entering numbers in the right place. A software subscription, office rent, advertising cost, insurance premium, loan payment, equipment purchase, and professional fee are not the same; each has a different accounting treatment and a different tax impact.

Misclassifying expenses distorts the reality of your profit and loss statement. And when you need to make a strategic decision, hire, cut costs, or get financing, you’re working with flawed data.

TaxLegit Tip: Build a clean, consistent chart of accounts from day one. A well-designed chart of accounts is the foundation that lets your CPA, bookkeeper, and business owner speak the same financial language and catch errors before they compound.

Have Questions?

Issue #6: Are You Making Business Decisions Without Reliable Financial Reports?

If the last time you reviewed your profit & loss was April 15th, then for the remaining eleven months of the year, you were making business decisions without current data. That’s the most expensive form of guessing there is.

Bookkeeping should help you run your business, not just file taxes. Six core financial reports give you the real-time picture you need to make confident decisions:

| Report | The Question It Answers | Why It Matters Right Now |

| Profit & Loss | Are we actually making money? | Catch margin erosion before it becomes a crisis |

| Balance Sheet | Where is our cash tied up? | Understand your true financial position, not just cash balance |

| Cash Flow Statement | Will we have enough cash next month? | Prevent payroll shortfalls and missed vendor payments |

| Accounts Receivable | Which clients are late on their bills? | Protect cash flow; act on overdue invoices early |

| Accounts Payable | What do we owe, and when is it due? | Avoid late-payment penalties and vendor-relationship damage |

| Payroll Summary | What are our true team costs? | Identify overtime trends, contractor costs, and benefits load |

| “The single most common mistake I see among growing businesses is treating financial reporting as a tax function rather than a management function. By the time the numbers reach your CPA, the opportunity to act on them is six months gone.”- Mike, CFO Advisor and author of Financial Clarity for Founders |

| Not Sure Where Your Books Stand?Tell us your situation in one line. Our compliance team will review your setup and recommend a clear path forward—free, in under 15 minutes.📅 Book Free 15-Min Consultation at TaxLegit.com | 📞 +91 8929218091 |

Practical Monthly Bookkeeping Checklist for US Small Businesses

Sarah, print this out and stick it on your wall. If every item on this list gets done consistently, the six issues above largely take care of themselves.

| Task | Frequency | Why It Matters |

| Upload receipts and invoices | Weekly | Prevents missing records at year-end |

| Reconcile bank accounts | Monthly | Catches errors and duplicate entries early |

| Reconcile credit card statements | Monthly | Tracks real expenses, not just bank transactions |

| Review unpaid invoices (AR) | Monthly | Improves cash flow and collections |

| Review vendor bills (AP) | Monthly | Avoids late payment penalties |

| Match payroll reports to books | Every payroll cycle | Prevents payroll recording errors before they compound |

| Review the Profit & Loss statement | Monthly | Understand true profitability, not gut feelings. |

| Review Balance Sheet | Monthly | Check business financial health at a glance |

| Share books with the CPA. | Quarterly | Avoid tax season pressure and late-filing penalties |

How TaxLegit Helps US Small Businesses

At TaxLegit, we provide clean, decision-ready books for business owners, CPAs, and growing companies. Backed by 15+ years of experience and trusted by 500+ clients globally, we look beyond the numbers to understand the business behind every transaction.

- Monthly Bookkeeping: Bank and credit card reconciliation, expense categorization, and ledger maintenance done accurately and on time.

- Payroll Coordination: Accounts payable/receivable tracking and payroll coordination that stays connected to your books in real time.

- Tax & Growth Readiness: Year-end cleanup, financial reporting, and CPA-ready books so tax season never becomes a crisis.

- Specialized US Business Support: Accounting support built specifically for US-based businesses and CPA firms, with multi-state compliance expertise.

A Final Thought from the Founder of Taxlegit

Throughout my career, I’ve seen bookkeeping dismissed as just another back-office chore. But the truth is, it quietly controls the fate of your company. When your books are clean, you aren’t guessing you know your true profit. Organized records turn tax season from a nightmare into a routine. Reliable numbers take the terrifying risk out of scaling.

For small business owners like Sarah, bookkeeping shouldn’t be a year-end burden. It must be a monthly habit. Because in the end, a business that truly understands its numbers is unstoppable.

Your Next Step

If Sarah’s situation sounds familiar, the best time to fix your books was six months ago. The second-best time is today. The right bookkeeping partner handles the cleanup, sets up a clean system, and makes sure you never face a tax season scramble again.

| Book a free 15-minute consultation at TaxLegit and get a clear bookkeeping action plan ( no commitment required )Visit taxlegit.com or WhatsApp us at +91 8929218091 to get started today. |

Disclaimer: This article is for informational purposes only and does not constitute formal legal, accounting, or tax advice. Federal and state tax laws change frequently. Always consult a qualified CPA or professional tax advisor regarding your specific business situation.

Frequently Asked Questions

Delaying bookkeeping until tax season. When records are updated late, receipts go missing, transactions get misclassified, and financial reports become unreliable. The IRS flagged over $1 billion in underpayment penalties in 2024 linked to this exact pattern.

Receipts and invoices should be uploaded weekly. Books should be reviewed and reconciled monthly. Waiting until year-end means you’re making business decisions for 12 months without reliable data and spending significantly more time on cleanup.

No, Bookkeeping is the foundation for cash flow management, profit tracking, loan applications, investor reporting, payroll accuracy, and business planning. If you’re only looking at your books at tax time, you’re missing 11 months of financial intelligence.

Yes, in the early stage. But as transactions, employees, contractors, and multi-state tax requirements increase, DIY bookkeeping creates compounding risk. Most business owners doing $500K+ in revenue find that the cost of professional bookkeeping is far lower than the cost of errors, penalties, and lost time.

Bank reconciliation matches your accounting records with actual bank activity. It catches missing entries, duplicate transactions, bank fees, failed payments, and recording errors.

About the Author

Srijita

Content Writer

Srijita is a legal and financial content specialist with 5+ years of experience in the Indian corporate sector. She simplifies MCA regulations and tax compliance into clear, actionable insights for entrepreneurs, working closely with Chartered Accountants and legal experts to ensure accuracy and compliance. Reviewed by Vipul Sharma, Co-Founder, Taxlegit.